Software supply chain risk is now a documented obligation. Can you attest to yours?

of large companies by revenue now formally name third party and supply chain risk their greatest cyber challenge, up from 54 percent.

of breaches now involve a third party or supply chain compromise. The share doubled in a single year, faster than most risk programs.

average time to contain a supply chain breach, the longest of any vector and the longest your attestations stay materially at risk.

median time from CVE disclosure to first observed exploit. Annual vendor questionnaires cannot evidence a control that turns over weekly.

Software supply chain risk is no longer a vendor questionnaire. It is a named, evidenced control.

For years the third party software risk question lived inside an annual vendor questionnaire and a paragraph in a SOC 2 report. Engineering owned the components, security owned the scanning, and your program owned the paperwork. That arrangement worked when the regulator did not name software dependencies, the auditor did not test the control, and the board did not ask for a number.

That world is gone. SEC cyber disclosure rules now require material incidents on the record within four business days. EU NIS2 and DORA name third party ICT and software supply chain risk as an explicit governance obligation with personal accountability. PCI DSS 4.0 and HIPAA Security Rule updates introduce specific software supply chain controls. Federal contractors carry executive order obligations on SBOM and provenance. Audit committees and risk committees now expect a current residual risk number with a trend, not a control narrative.

A vendor questionnaire answered annually

A continuous control with daily evidence

A control narrative in a SOC 2 report

A tested control with sampled evidence

A footnote on the risk register

A top tier risk with a residual score

An assurance to the risk committee

A score, a trend, and an evidence packet

This guide is to give you the evidence trail behind a control you already attest to.

The compliance questions you cannot evidence yet.

These are not security questions. They are the questions you get asked at a regulatory examination, an internal audit walkthrough, a SOC 2 readiness, a risk committee meeting, or a vendor due diligence response. Read each one and ask yourself honestly whether you could evidence it today, with a current artifact, not from a control narrative and not from a promise to follow up.

At your next regulatory examination, can you produce continuous evidence of your software supply chain controls?

What is your residual software supply chain risk today, expressed as a number?

When a CVE surfaces in a component your product or your vendor uses, how long until you know, and how long until you can attest?

When customer security reviews and RFPs ask for your SBOM, vendor risk artifacts, and continuous monitoring evidence, can your team respond in hours, not weeks?

What is the cumulative exposure of an unevidenced software supply chain control on your program today?

The cost is rarely one event. It is the regulatory finding that lands in the examination report because the control operated but could not be evidenced. It is the SOC 2 or ISO 27001 qualification that downgrades your customer trust profile for the year. It is the breach notification timeline you missed by hours because the inventory was stale. It is the enterprise contract that paused in security review because the SBOM was not current. It is the personal accountability obligation under NIS2 or DORA that names the executive on the signature line. None of these are catastrophic on their own. Together they are the picture of a program that did not keep pace with the obligation.

The same blind spot, in the three rooms where you have to attest.

The underlying gap is the same in each room. What changes is who is in the room with you, and what is on the line when the control gets tested. As Chief Risk or Chief Compliance Officer you carry all three.

Your regulator wants evidence of a control, not a description of one.

Modern enterprise MSAs include security representations, third party software warranties, audit rights, and breach notification clocks measured in hours. Your team negotiates the language, but the evidence behind it sits in repos you do not read. Without a continuous artifact, every signature is a future dispute waiting on a trigger event.

Your internal and external auditors want a tested control with sampled evidence.

An incident occurs. The SEC clock, the state law clock, and the contractual clock all start at the same moment, on different timers. You are the one signing the notice letters, advising the disclosure committee, and coordinating with insurance counsel. A current SBOM and risk score is the difference between a defensible notification and a regulatory enforcement matter.

Your board and audit committee want a residual risk number, not assurance.

Sophisticated buyers test the technical reps against the repositories themselves. Anything the seller could not see in advance becomes a re-price lever, an escrow, or a survival extension. The General Counsel who walks in with a documented score and inventory walks out with closing on the original terms.

And under NIS2 and DORA, the signature line names a person, not a department.

EU NIS2 and DORA, SEC cyber disclosure rules, and a growing list of state regulators now name individual executive accountability for cyber and supply chain risk governance. When the examination, the audit, or the breach inquiry asks who attested to the control, the question comes to a person, not a program. This guide exists so that when it does, you can put a score, a trend, and an evidence trail on the table, rather than a description of intent.

Three authorities. Three independent voices. One conclusion.

These are not vendors. They are the federal regulator, the global standards body, and the board governance association. When the bodies that examine you, define your controls, and oversee your directors all describe the same shift in the same year, the shift is the consensus, not a marketing claim.

Public companies must disclose material cybersecurity incidents within four business days and describe their cybersecurity risk management, strategy, and governance, including oversight of risks from third party service providers.

U.S. Securities and Exchange Commission

Cybersecurity Disclosure Rules, in effect

Organizations should identify, prioritize, assess, respond to, and monitor cybersecurity risks arising from suppliers, their products and services, and other third parties. Software supply chain risk is now an explicit governance category.

National Institute of Standards and Technology

NIST Cybersecurity Framework 2.0, Govern function

Enterprise risk management programs must treat software and third party supply chain exposure as a top tier risk, with continuous monitoring, documented evidence, and named accountability replacing periodic vendor assessment as the baseline standard.

ISACA

Global professional association for governance, risk, audit, and compliance leaders

What an unevidenced control has cost the programs that ran them.

None of these are worst case scenarios. They are documented averages drawn from independent research, government reporting, and standards bodies. The point is not fear. The point is that the cost is real, measurable, and already being paid by compliance programs that assumed the questionnaire was the evidence.

Now run the math on your own program.

The ledger above shows industry averages. Plug in your audit scope, your regulatory footprint, and your customer review volume, and see what an unevidenced control is actually costing your program.

None of this asks you to evaluate a security tool. It asks you to put evidence behind a control you already attest to.

Every consequence above traces back to the same root cause. The control existed on paper, the threat moved faster than the cycle, and no one in a position of program accountability could put a current artifact on the table when the regulator, the auditor, or the committee asked. The fix is not a larger security organization. It is continuous, evidence grade visibility into a control you already own, so it becomes a number and an artifact pack you bring to the room instead of a finding someone else brings to you. That is the entire reason TripleKey exists.

The math your program will run anyway.

You will evidence this control eventually, either by running a continuous program or by absorbing the findings, the qualifications, and the delays. These are the four lines a Chief Risk or Compliance Officer usually adds together. Each one on its own exceeds the annual cost of TripleKey. The combined total is not a question of return, it is a question of magnitude.

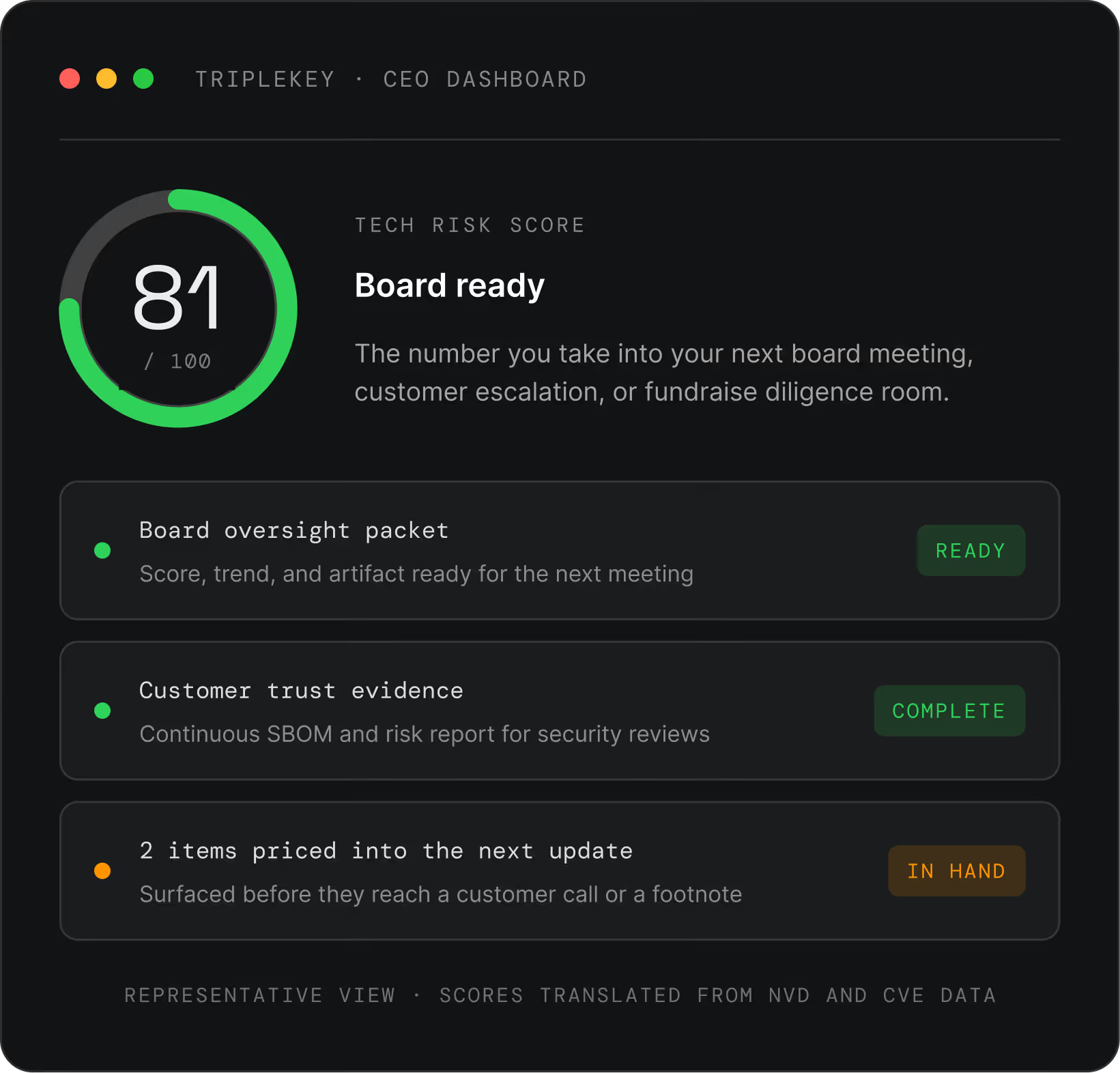

One score, one artifact pack, ready for any examiner, auditor, or risk committee.

TripleScan continuously scans your codebase and the components it depends on, then translates everything it finds into a single Tech Risk Score from 0 to 100 with a dated evidence trail behind it. You do not read code. You read the score and pull the artifact pack, the same way you read a risk register, and you walk into the examination, the audit walkthrough, or the risk committee with the evidence ready.

You ask for the evidence. Your engineer produces the data.

Getting your first risk score and evidence pack does not require you to touch a line of code. Your job is to start the trial and own the attestation. The technical work belongs to the person who already owns the codebase.

01/03 You sign up

02/03 Engineering connects it

03/03 You get the artifact pack

Residual Risk Score

Continuous SBOM

Control Evidence Pack

Walk into the next examination with the evidence.

The next time your regulator, your auditor, or your board risk committee asks whether you can evidence your software supply chain control, have the score and the artifact pack ready instead of a narrative. Start a free trial, invite your engineering lead, and see exactly where you stand.